Protective Put Explained: How to Hedge Stock Losses

After a strong multi-year run in the stock market, it is natural to want to take chips off the table. Lock in gains. Get out before it all unravels.

The story is seductive.

Buy low. Sell high. Avoid the crash. Everyone knows the horror stories of 50% drawdowns. No one wants to be that sucker.

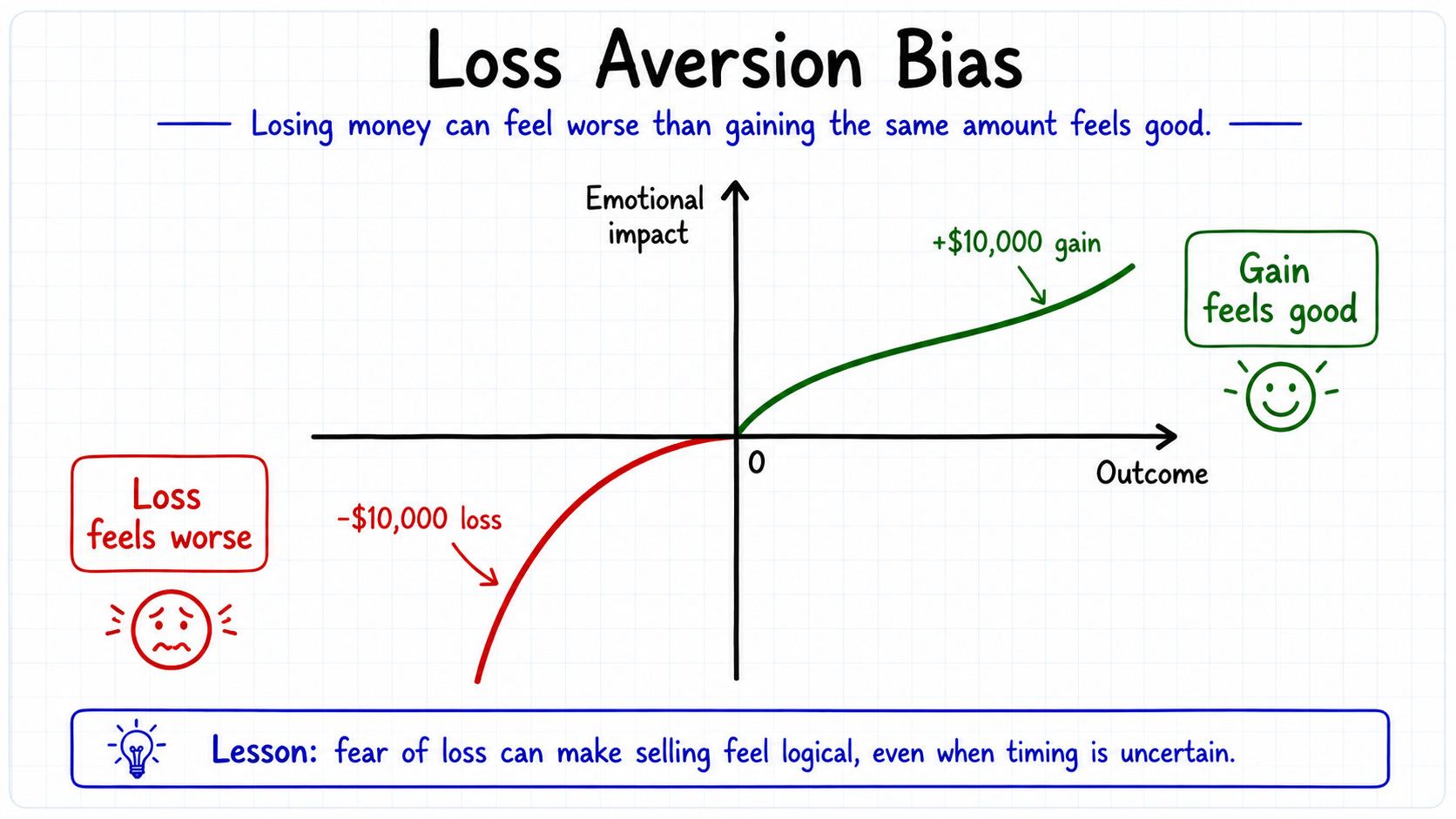

Loss aversion is powerful. Losing money often feels much worse than making the same amount feels good. That fear can make selling feel like discipline. It can make “getting out before the crash” feel smart and controlled.

But fear can also push you into bad decisions at exactly the wrong time.

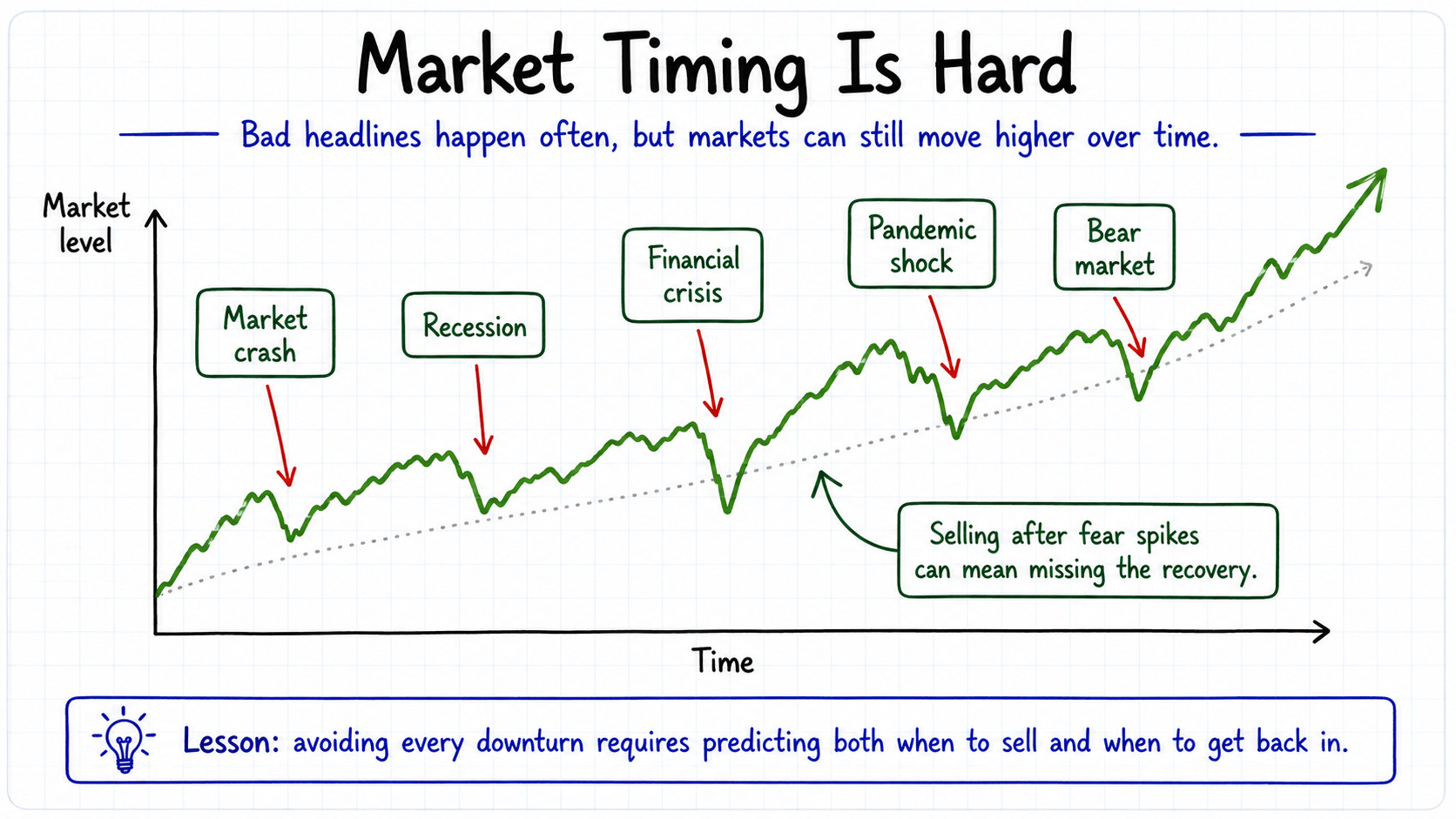

If timing the market were easy, everyone would do it. The problem is that market timing rarely works the way investors hope. Some of the market’s best days have happened close to its worst days. That means investors who sell to avoid the bad days may also miss the good days that often follow. Missing only a few strong days can have a large impact on long-term returns.

Now suppose you believe the stock market may fall soon. Should you sell all your stocks? Usually, that is not a simple or reliable solution.

The market could keep rising after you sell. If you sell investments in a taxable account, you may also create a tax bill. And once you are out of the market, you still have to decide when to get back in.

That puts you right back in the same hard position: playing with your crystal ball.

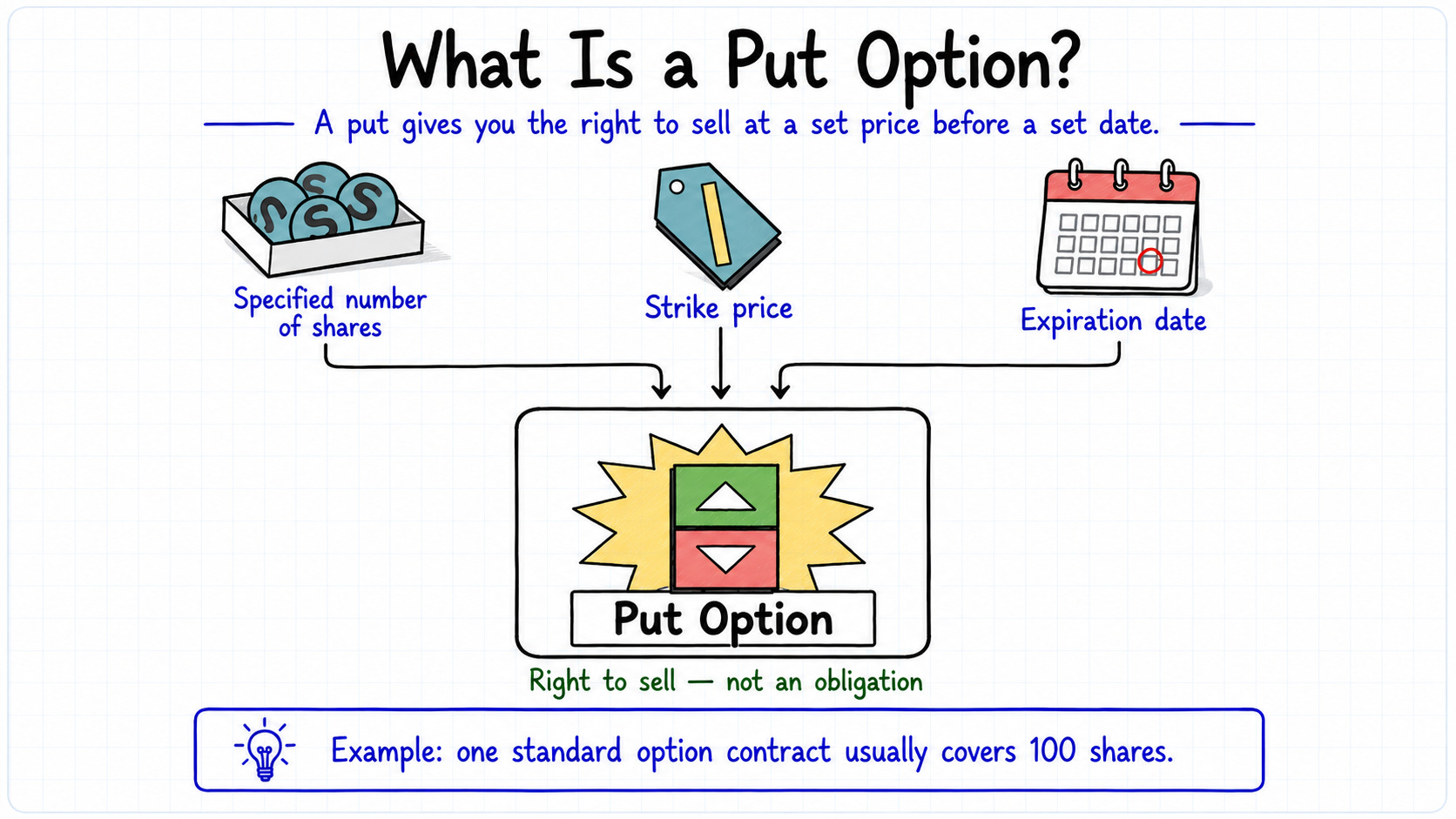

One possible risk-management tool is a protective put.

A protective put is an options strategy. It means you keep owning the stock or fund, but you also buy a put option on that same investment. A put option gives you the right, but not the obligation, to sell the investment at a set price before a set date.

Think of it like insurance on part of your portfolio. You pay a cost upfront, called the option premium. In exchange, the put can help limit losses if the investment falls below the option’s strike price before the option expires.

A protective put is different from selling your investments and moving to cash. With a protective put, you still own the investment, so you can still benefit if it rises. But the protection is not free. The cost of the put reduces your return, and that cost can be meaningful, especially if you use this strategy often.

If the market falls, the put option can gain value as the investment loses value. That gain can help offset some or all of the loss below the strike price, depending on the option terms, timing, taxes, and trading costs.

Put simply, a protective put can help set a temporary floor under your losses.

This does not make protective puts simple or risk-free. Options expire. They can be expensive. Choosing the wrong strike price or expiration date can make the protection less useful than expected.

For many investors, this is exactly the kind of decision that should be made with help from a qualified financial advisor.

Example of a Protective Put

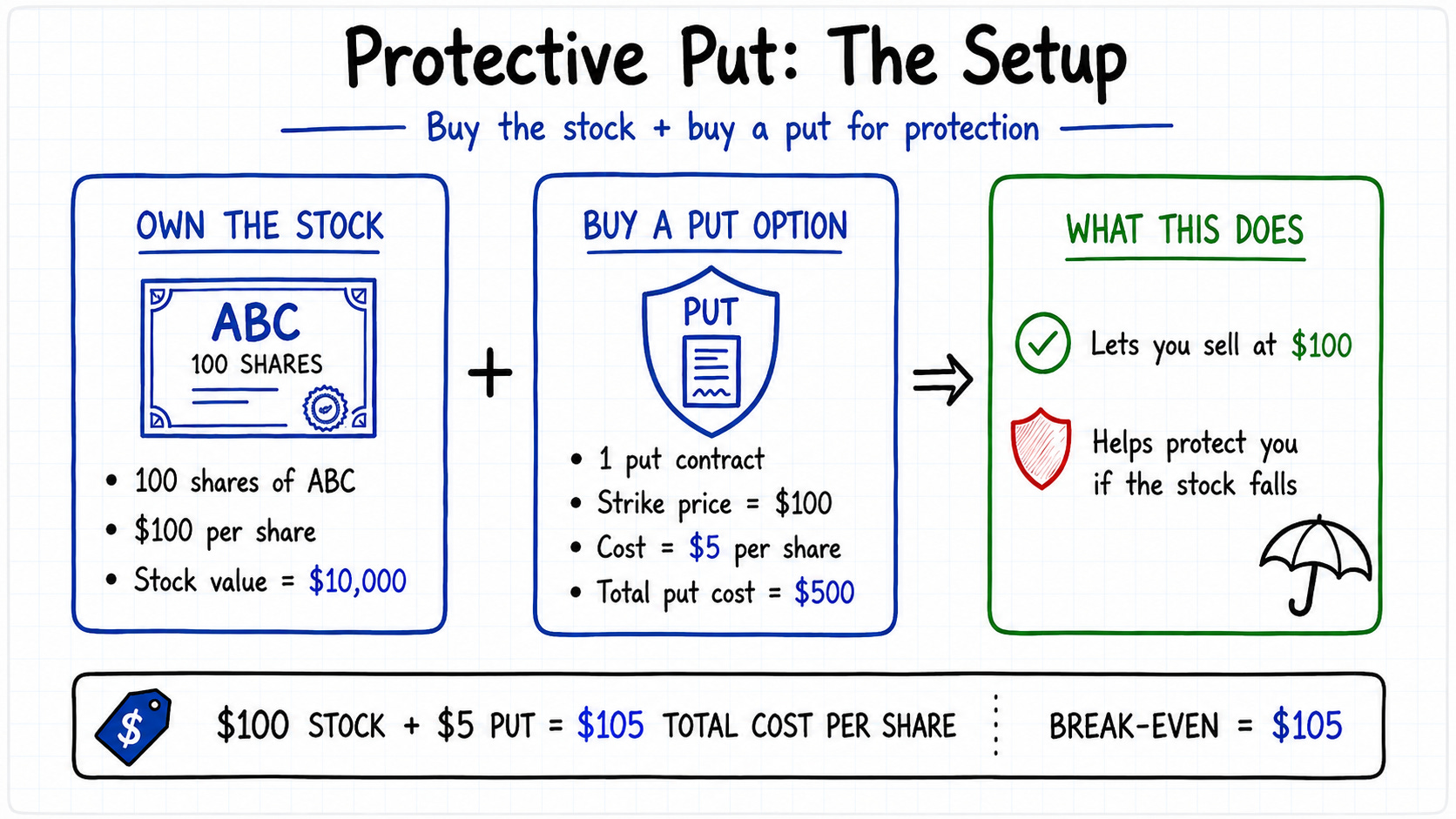

Suppose you own 100 shares of ABC Corp. Each share is worth $100, so your total stock position is worth $10,000.

You believe the stock price may rise over time. But you also want protection in case the price falls unexpectedly. To reduce that risk, you buy one put option with a $100 strike price. One standard put option contract usually covers 100 shares.

The put costs $5 per share. Since the contract covers 100 shares, the total cost is $500.

In this example, your total cost is now $105 per share:

$100 for the stock

+ $5 for the put option

= $105 total cost per share

That means your break-even price is $105. You do not make a profit unless the stock rises above $105 before the option expires.

The result depends on where ABC Corp’s stock price is when the option expires. Here are three possible outcomes.

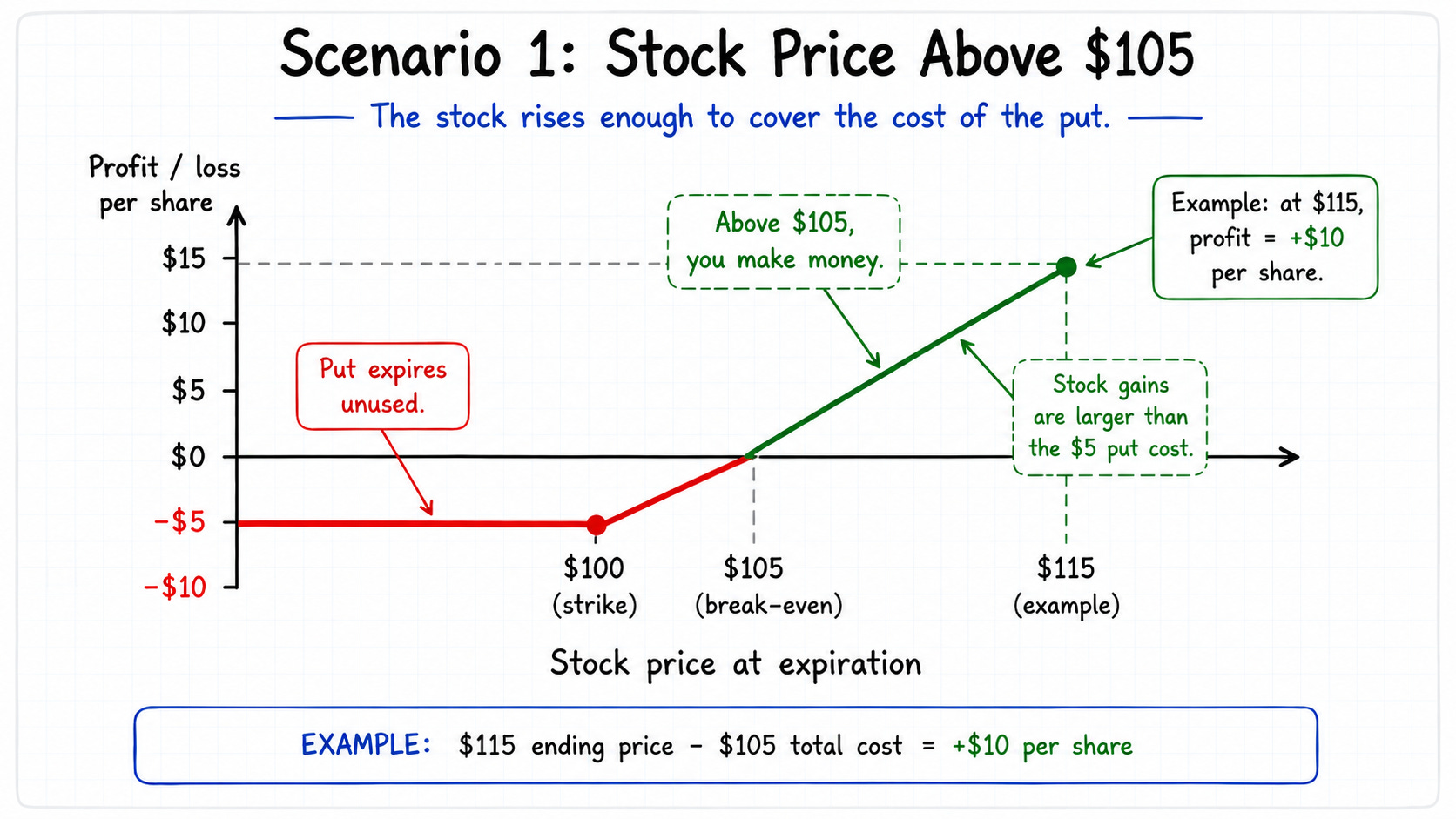

Scenario 1: The stock price is above $105

If ABC Corp rises above $105, your stock has gained enough to cover the cost of the put option.

For example, if the stock rises to $115, your gain is:

$115 current stock price

$105 total cost per share

= $10 profit per share

In this case, the put option would usually expire unused because you would not need to sell your shares at $100 when the market price is higher.

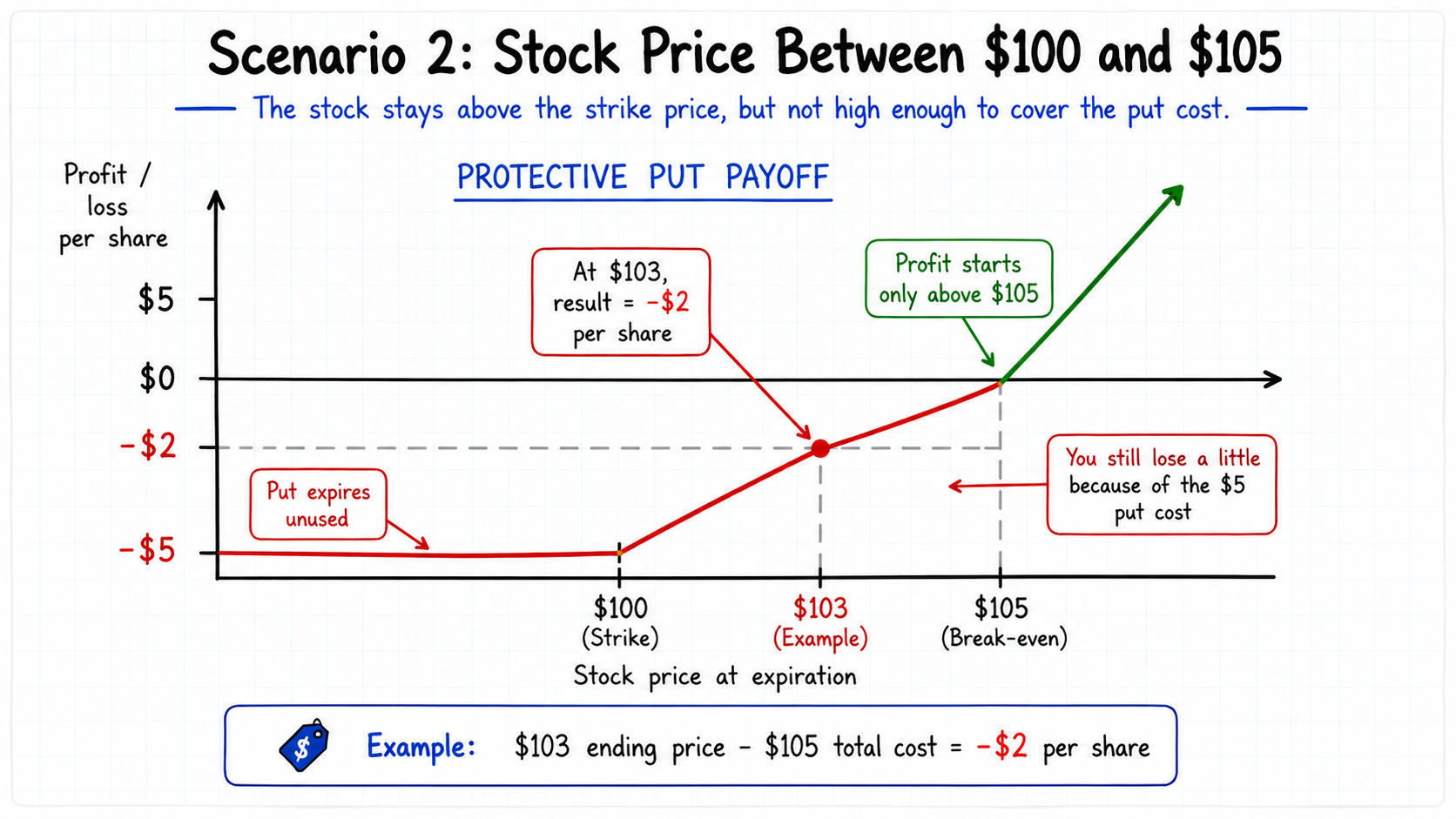

Scenario 2: The stock price is between $100 and $105

If the stock price ends between $100 and $105, your shares are worth the same or slightly more than before. But you still paid $5 per share for the put option.

Because of that cost, you may still have a small loss.

For example, if the stock price is $103, your result is:

$103 current stock price

$105 total cost per share

= $2 loss per share

The put option would usually expire unused because the stock is still trading above the $100 strike price.

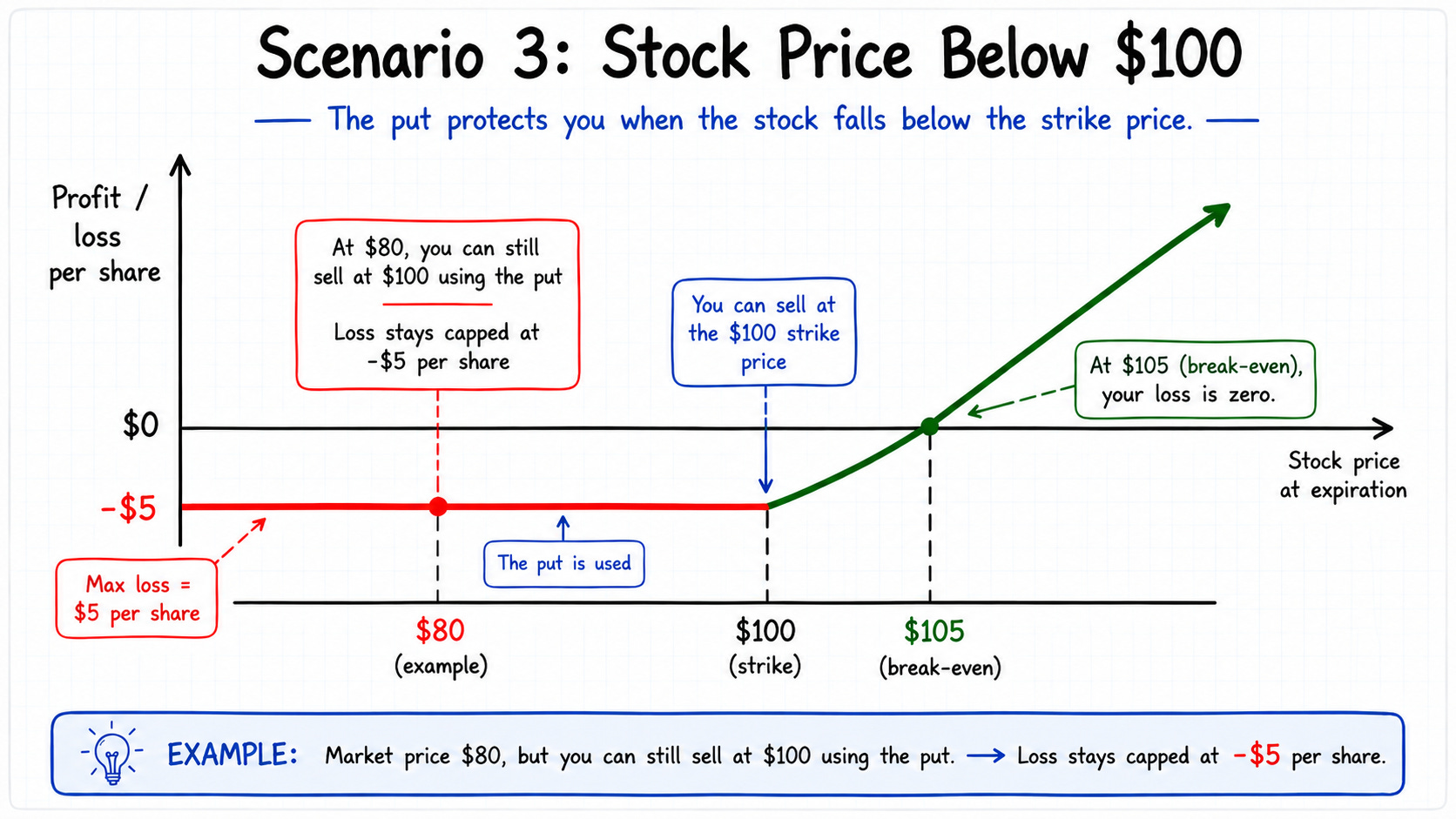

Scenario 3: The stock price is below $100

If the stock price falls below $100, the put option can help protect you. The put gives you the right to sell your 100 shares at $100, even if the market price is lower.

For example, if the stock falls to $80, you could still use the put to sell your shares at $100.

In this simple example, your stock sale price would be $100 per share. Since you paid $100 for the stock and $5 for the put, your loss would be limited to $5 per share, or $500 total, before taxes and trading costs.

This is the main purpose of a protective put: it can limit downside risk for a set period of time while allowing you to keep potential upside if the stock rises. But the protection is not free, and the option only protects you until it expires.

When Protective Puts Can Make Sense

Protective puts are easiest to understand when you stop thinking about them as “options trades” and start thinking about them as temporary insurance.

You are not trying to get rich from the put. You are not betting against your own portfolio. You are paying a known cost to protect against a risk you cannot afford to ignore.

That can make sense in three common situations.

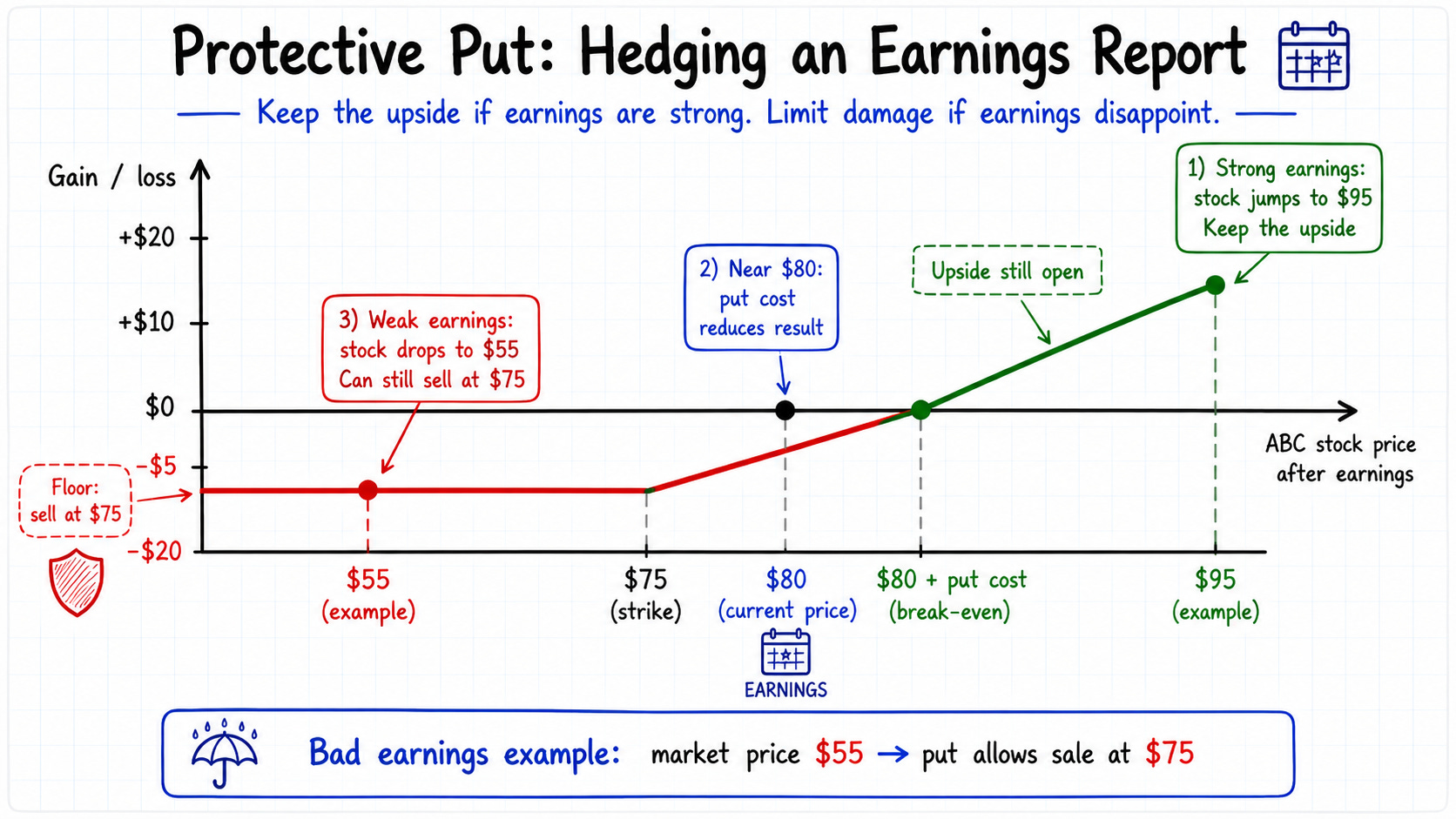

Protective Put Example 1: Hedging an Earnings Report

Suppose you own 100 shares of ABC Corp at $80 per share. You like the company. You believe the long-term story is still strong. But earnings are coming next week, and you know the stock could move sharply in either direction.

You do not want to sell. Selling could trigger taxes. It could also force you to guess when to buy back in. But doing nothing feels reckless.

So you buy one put option with a $75 strike price that expires in one month.

That put gives you the right to sell your 100 shares at $75, even if the stock falls much lower after earnings.

If ABC reports strong numbers and the stock jumps to $95, you keep the upside. The put will likely expire unused. Your only cost is the premium you paid for the protection.

If ABC disappoints and the stock falls to $55, the put becomes valuable. Instead of watching the full loss hit your account, you have the right to sell at $75. The put does not make the bad news disappear. It simply helps limit the damage.

That is the tradeoff. You pay a cost upfront so one bad earnings report does not wreck your position.

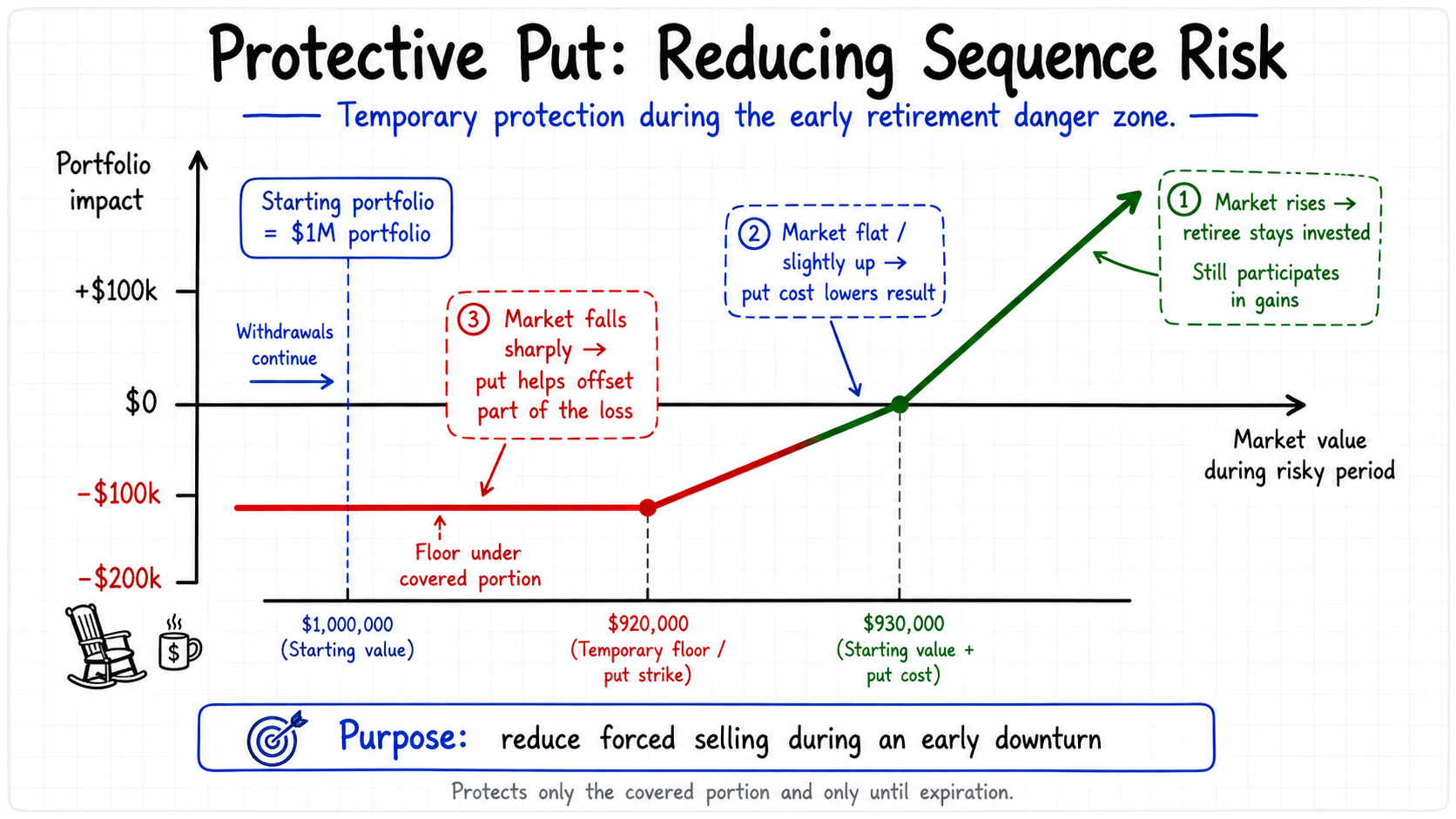

Protective Put Example 2: Reducing Sequence Risk for a New Retiree

Now suppose you just retired with a $1 million portfolio. You plan to use the portfolio for income. You also know the first few years of retirement matter a lot.

Why? Because large market losses early in retirement can be especially painful. If your portfolio falls while you are also taking withdrawals, you may be forced to sell investments when prices are down. That can make it harder for the portfolio to recover later.

This is called sequence of return risk. The name is technical. The idea is simple.

Bad returns are always unpleasant. Bad returns early in retirement can be dangerous.

A protective put may help reduce that risk for a limited period. For example, a retiree with a large S&P 500 ETF position could buy put options on that ETF before a risky stretch in the market.

The puts would not protect the entire retirement plan from every possible problem. They would not remove the need for cash reserves, smart withdrawals, or proper diversification.

But they may help create a temporary floor under part of the portfolio.

If the market rises, the retiree stays invested and participates in the gains, minus the cost of the puts. If the market falls sharply, the puts can help offset part of the loss.

For a new retiree, that can be the difference between staying calm and making a fear-based decision. It can also give the advisor more room to manage withdrawals, taxes, and rebalancing without being forced to sell stocks during a panic.

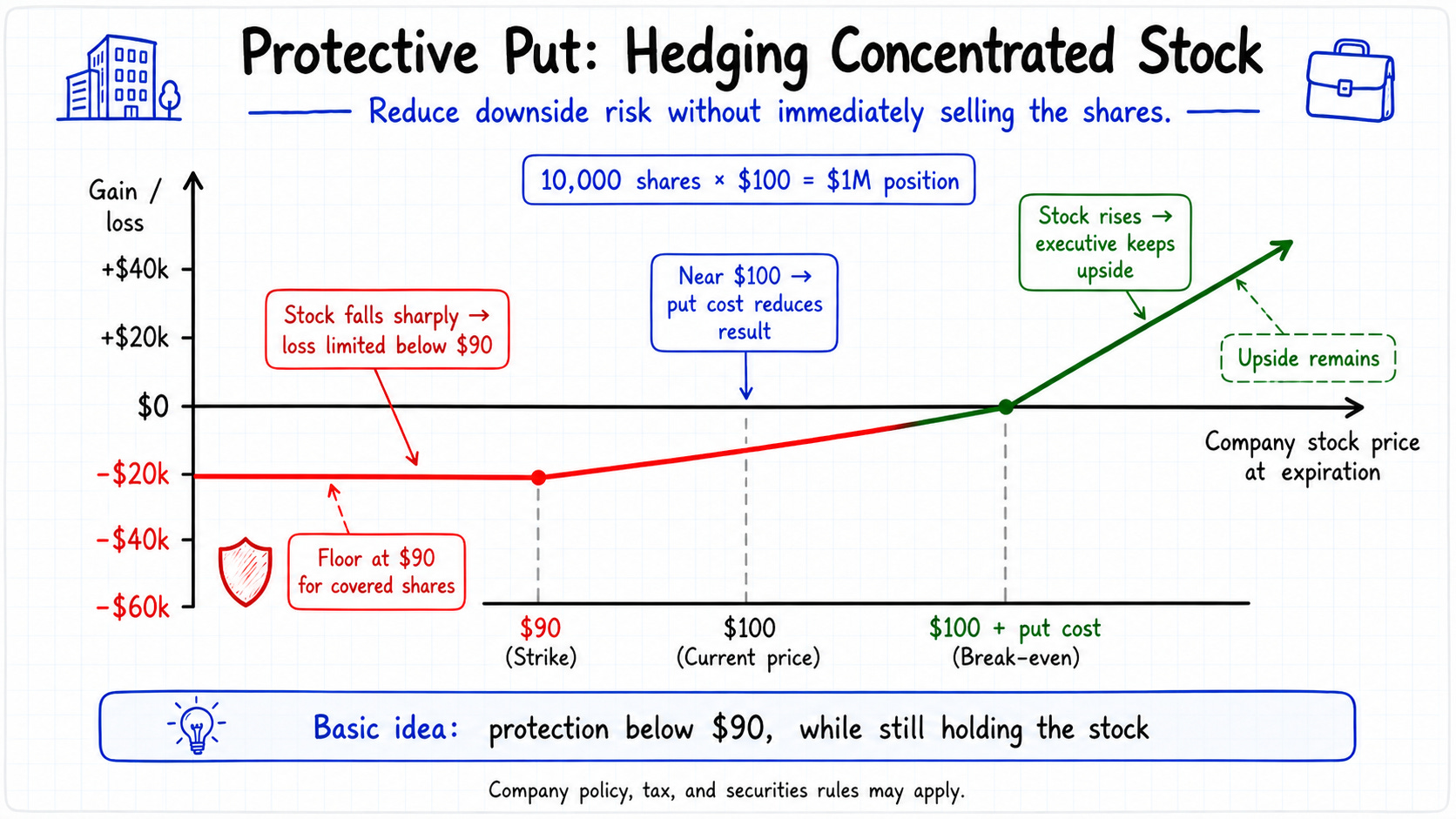

Protective Put Example 3: Hedging a Concentrated Company Stock Position

Now consider an executive who owns a large amount of company stock.

Maybe the stock came from years of equity compensation. Maybe it has grown into the largest part of the executive’s net worth. On paper, this looks like success. In real life, it can be a serious risk.

The executive’s salary, bonus, benefits, and stock wealth may all depend on the same company. If the company has a bad year, the executive could face job risk and portfolio losses at the same time.

Selling the stock may not be easy. There may be trading windows, company rules, tax issues, or personal reasons to hold the shares. But doing nothing can leave too much wealth tied to one company.

A protective put can help manage that risk.

Suppose an executive owns 10,000 shares of company stock at $100 per share. That is a $1 million position. The executive still believes in the company, but wants protection before a major product announcement or earnings report.

The executive could buy put options with a $90 strike price. If the stock rises, the executive still owns the shares and keeps the upside, minus the cost of the puts. If the stock falls sharply, the puts can help limit the loss below $90 for the covered shares.

This does not solve every problem. The puts cost money. They expire. They may need to be approved under company policy. They may also create tax, securities law, or insider trading concerns that require professional guidance.

But the basic idea is simple: the executive can reduce downside risk without immediately selling the stock.

That is where protective puts can be useful. Not as a magic trick. Not as a prediction tool. Not as a way to avoid planning.

They are a tool for specific risks, over specific time periods, when selling may create problems of its own.

Used poorly, protective puts can become expensive and confusing. Used carefully, with the right advisor, they can help investors stay invested without pretending risk does not exist.

Protective Put FAQs

1) Is a protective put worth the cost?

Sometimes. But not always.

A protective put is like insurance. You pay a premium to limit a specific risk for a specific period of time. That cost reduces your return if the stock goes up, stays flat, or does not fall enough for the put to help.

That does not make it a bad tool. It means the tool needs a purpose.

Protective puts can make sense when the risk is large, temporary, and worth paying to reduce. They usually do not make sense as a permanent strategy on every investment you own. Used too often, the cost can quietly eat into your returns.

2) How do I choose the strike price and expiration date?

The strike price is the price where your protection starts. The expiration date is when that protection ends.

A strike price close to the current stock price gives more protection, but it usually costs more. A lower strike price costs less, but it leaves you exposed to more losses before the protection helps.

The expiration date should match the risk you are trying to manage. If you are worried about an earnings report next month, you probably do not need protection for several years. If you are hedging a major retirement or tax-planning risk, the time frame may be longer.

This is where investors can get into trouble. The put can be the right idea, but the wrong strike price or expiration date can make it expensive and ineffective.

3) Should I buy protective puts on every stock I own?

Usually, no.

Buying puts on every holding can get expensive fast. It may also add more complexity than value.

Protective puts are usually better used on the risks that matter most. That might be a large single-stock position, a major market risk before retirement withdrawals begin, or a stock you cannot easily sell because of taxes, company rules, or timing.

The goal is not to insure everything. The goal is to protect the risks that could seriously damage your plan.

4) What are the downsides of protective puts?

Protective puts are not free. They are not simple. And they are not magic.

The biggest downside is cost. If the stock rises or stays flat, the put may expire worthless. That means you paid for protection you did not end up using.

There are other risks too. Options expire. Prices can move quickly. The put may not protect as much as you expected. Taxes and trading costs can also change the real result.

The biggest behavioral risk is overconfidence. Some investors buy protection and then take more risk than they should. That defeats the purpose.

A protective put can reduce downside risk. It does not remove the need for diversification, cash reserves, tax planning, and disciplined decision-making.

5) How do protective puts fit into a financial plan?

A protective put should be part of a plan, not a replacement for one.

It may help when you want to stay invested but also want to limit losses during a specific risk window. That could mean protecting a concentrated stock position, reducing market risk near retirement, or managing a short-term event like earnings.

But the first question is not, “Which option should I buy?”

The first question is, “What risk are we trying to reduce?”

From there, the right answer may be a protective put. It may be a collar. It may be selling part of the position, building cash, diversifying, or doing nothing.

Protective puts can be useful. Used poorly, they are just an expensive way to feel safer. Used carefully, they can help investors stay invested without pretending risk does not exist.